Last updated on August 3rd, 2022 at 08:22 pm

GST on Brick Kilns Sector

The compliance burden and the outflow towards the GST liability have increased considerably with the implementation of the recommendation of the 45th GST Council Meeting.

- A revised tax rate structure for the specified goods of the Brick Kilns Sector has been notified.

- The benefit to pay tax at a lower rate and fewer GST compliances has been withdrawn for the traders as well as the manufacturers of the Bricks Industry.

- The threshold limit to obtain registration under the GST regime for the brick manufacturing and brick trading industry was revised to Rs 20 Lakhs from Rs 40 lakhs. – CGST Ntf no. 3 dated 31.03.2022 read with section 22.

- Condition of 90% or more fly ash content applied only to Fly Ash Aggregates has been omitted w.e.f 18th July 2022.

Specified Goods of the Brick Kilns Sector

Notified vide CGST(Rate) Notification no. 02/2022 dated 31.03.2022 {Effective date – 01.04.2022}

Amended vide CGST(Rate) Notification no. 10/2022 dated 13.07.2022 {Effective date – 18.07.2022}

Clarification vide CGST Circular no. 179/2022 dated 03.08.2022 {Effective date – 18.07.2022}

[su_table]

| HSN Code | Description of Goods |

|

6815 |

Fly ash bricks; Fly ash aggregates; Fly ash blocks (Circular clarifying the % of ash content) |

|

69010010 |

Bricks of fossil meals or similar siliceous earth |

|

69041000 |

Building bricks |

|

69051000 |

Earthen or roofing tiles |

[/su_table]

GST Rate & ITC of the Brick Kilns Sector

[su_table]

| Category of Taxpayer | From 01.04.2022 | Up to 31.03.2022 |

| GST registration is required as AATO does not exceed the threshold limit | The threshold limit reduced to Rs 20 Lakhs | The threshold limit is Rs 40 Lakhs |

| Taxpayer opts for Composition Scheme | Composition levy is not permitted for specified goods above |

GST Rate @ 1% If AATO does not exceed Rs 1.5 Crores ITC cannot be availed by the supplier or recipient. |

| Taxpayer registered as a regular taxpayer (QRMP or Non-QRMP) | GST rate @ 12%

{CGST(Rate) Ntf no. 1 dated 31.03.2022} ITC can be availed and the recipient can avail of the ITC. |

GST rate @ 5%.

ITC can be availed and the recipient can avail of the ITC. |

| GST rate @ 6%

{CGST(Rate) Ntf no. 2 dated 31.03.2022} {CGST(Rate) Ntf no. 10 dated 13.07.2022} ITC cannot be availed but the recipient can avail of the ITC. |

[/su_table]

Note: As per section 17(2) of CGST Act,2017 – ITC will be blocked for other supplies as well, if the taxpayer opts to pay GST @ 6% and supplies other supplies along with the specified supplies above.

Note: Lower rate of 6% GST has been notified where the supplier can rightfully issue the tax invoice @ 6% and collect the tax from customers and deposit the GST with Revenue without availing any ITC. (Unlike the case of composition levy where lower rates like 1%, 2% & 5% are notified but the supplier cannot collect the tax from customers or avail any ITC)

Impact of the amendments made in the Brick Kilns Sector

[su_table]

|

Category of the taxpayer up to 31st March 2022 |

Category of the taxpayer from 1st April 2022 | |

| If you opt to pay GST @ 12% |

If you opt to pay GST @ 6% |

|

| Unregistered – If you were not required to register as AATO did not exceed the threshold limit | When you were not registered there can be no question of availing or reversal of ITC | When you were not registered there can be no question of availing or reversal of ITC |

| Composition Taxpayer – If the taxpayer had opted for the composition scheme and paid GST @ 1% | File application in Form GST CMP 04 to withdraw from the composition scheme.

File Form GST ITC 01 for availing the ITC on the transitional stock and capital goods. |

File application in Form GST CMP 04 to withdraw from the composition scheme.

When you opt for a lower GST rate then there is no question of availing or reversal of ITC. |

| Regular Taxpayer – If the taxpayer was registered as a regular taxpayer paid GST @ 5% | You can continue utilizing the balance in the ITC ledger.

There is no requirement for reversal of ITC. |

File Form GST ITC 03 for reversing the ITC on the transitional stock, and reversing the proportionate of capital goods |

[/su_table]

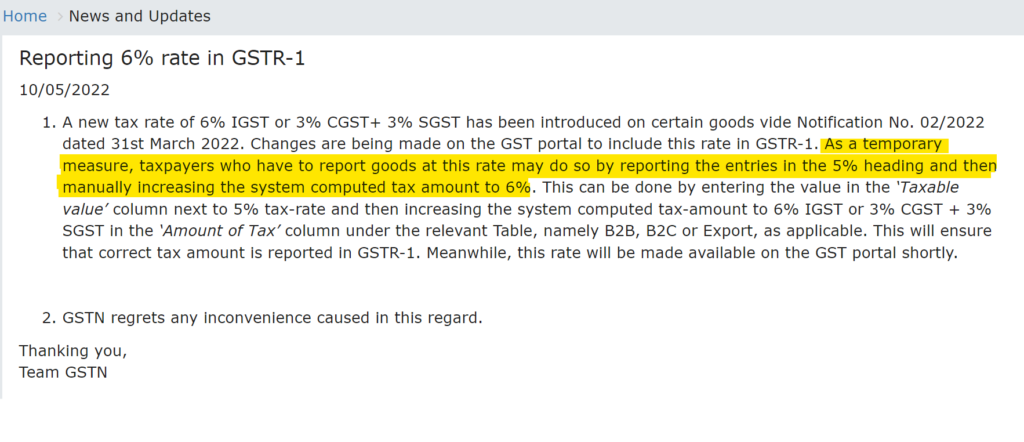

Temporary solution for Brick Kilns Sector dated 10th May 2022

As 6% GST rate was not available for reporting in GSTR 1 on GST Portal.

Taxpayers were asked to

📌 Select 5% GST Rate

📌 Then increase the system computed tax value in the “amount of tax” column with the values calculated @ 6 instead of 5%(system/auto-calculated)

Conclusion

Supplier (Manufacturer or Trader) who was not required to register as the threshold limit was Rs 40 Lakhs will now have to register as soon as the turnover crosses Rs 20 Lakhs.

If opts for 12% – As the supplier would directly jump from no applicability of GST @12%. Though the same will be collected from customers and paid to Revenue. But without setting off any ITC on the opening inventory as well as capital goods will be burning cash-out (As GST payments on opening inventory but later on, ITC will be available)

She can be contacted at info.financepost@gmail.com

- 50th GST Council Meeting - 11/07/2023

- GST Compliance Calendar of October 2023 - 01/04/2023

- GST sections amended in Finance Act 2023 - 27/03/2023

Disclaimer: The above content is for general info purpose only and does not constitute professional advice. The author/ website will not be liable for any inaccurate / incomplete information and any reliance you place on the content is strictly at your risk.

Follow us on Social Media by clicking below

Follow @financepost_in

Be the first to comment