Last updated on August 24th, 2022 at 06:54 pm

FAQs on rebate u/s 87A

Rebate u/s 87A refers to the relief from paying taxes for certain individuals. Till FY 2018-19, the resident individuals with a total taxable income of less than equal to Rs 3.5 lacs were able to claim the rebate of tax to the extent of Rs. 2,500.

In the Budget 2019, the Finance Minister increased the limit of rebate u/s 87A from Rs 2,500/- to Rs 12,500/-. Accordingly, the individuals with total income less than or equal to Rs. 5 lakhs shall be entitled to a deduction of an amount equal to 100% of such income tax or an amount of Rs. 12,500, whichever is less, from the amount of income tax on his total income which he is chargeable to tax.

Click here to understand the detailed provision and computation.

FAQs on Rebate

Q. Can NRI get the benefit of rebate u/s 87A?

Ans: As mentioned in section 87A of the Income Tax Act, only the Resident individuals are eligible to claim rebate u/s 87A. Hence a non-resident cannot take the benefit of Rebate u/s 87A.

Q. Can HUF claim Rebate u/s 87A?

Ans: No. Only the Resident individuals are eligible to claim rebate u/s 87A.

Q. Can Partnership Firm claim Rebate u/s 87A?

Ans: No. Only the Resident individuals are eligible to claim rebate u/s 87A.

Q: I am a resident Individual and my taxable income after deductions u/s 80 is Rs 4.5 lakh. The tax payable on this is Rs. 10,000. After taking the benefit of rebate u/s 87A my tax liability will be Nil. Can I avoid filing a tax return since I am not liable to pay tax?

Ans: No. The rebate u/s 87A is claimed by filing the tax return. The fact that your total income exceeds the minimum threshold of Rs 2,50,000/-, you are liable to file a tax return. In the tax return, you can claim the rebate of the entire tax payable of Rs. 10,000 and pay Nil tax or claim a refund for the tax already paid or deducted at the source if any.

Q. I am a resident individual and my taxable income after taking the benefit of all deductions is Rs. 5,08,000/- Can I get the benefit of rebate u/s 87A?

Ans: No. The rebate u/s 87A can be claimed only if your total income minus deductions is less than or equal to Rs. 5 lakh. In the above scenario, considering your income does not include capital gains, and you are below 60 years of age, you will have to pay taxes.

Q: I am a resident individual and my total income comprises of LTCG (other than equity shares) of Rs 5 lakh. What will my tax liability look like? Can I claim a rebate u/s 87A?

Ans: Yes. Since your total income chargeable to tax is exact Rs 5 lakh you satisfy the condition of total income less deduction equal to or less than Rs 5 lakh. However, your rebate will be restricted to Rs. 12,500. Your Tax liability will be as follows assuming you are less than 60 years old:

[su_table]

| Gross Total Income |

5,00,000 |

| Less: Deductions u/s 80 |

NIL |

|

Taxable income |

5,00,000 |

| Tax liability (@ 20% on LTCG) |

50,000 |

| Less: Rebate u/s 87A (Max) |

(12,500) |

|

Tax payable |

37,500 |

| Add: Cess @ 4% |

1,500 |

|

Total tax liability |

39,000 |

[/su_table]

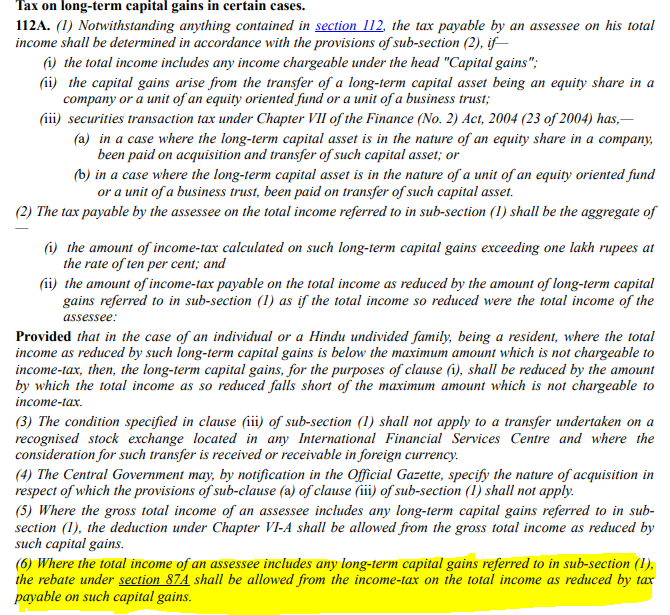

Q: I am a resident Individual and my income consists of the only LTCG from equity shares of Rs 5 lacs. Can I get the benefit of rebate u/s 87A?

Ans: No. The LTCG from equity shares is chargeable to tax u/s 112A from FY 2018-19. However, as mentioned in Sec112A,

Where the total income of an assessee includes any long-term capital gains on equity shares as mentioned in sub-section 1 of section 112A, the rebate under section 87A shall be allowed from the income tax on the total income as reduced by tax payable on such capital gains.

Hence, you cannot claim any rebate u/s 87A in such a scenario.

Q: I am a resident individual and my age is 84. Can I get the benefit of rebate u/s 87A?

Ans: The rebate u/s 87A can be claimed by any resident individual if his / her total taxable income minus deduction is equal to or less than Rs. 5 lakhs. The fact that you are super senior citizens, your taxable income up to Rs 5 lakhs attracts Nil tax (Refer tax slabs).

Rebate u/s 87A is irrelevant to super senior citizens.

Q. I am a 35 years old resident and salaried individual. My salary is Rs 10 lakhs p.a. I own two houses, one in Mumbai where I live and another in Jaipur. Can I reduce my tax liability to Nil?

Ans: The rebate u/s 87A can be claimed by any resident individual if his / her total taxable income minus deduction is equal to or less than Rs. 5 lakhs. Hence, If you plan appropriately and reduce your taxable income after deductions to Rs 5 lakhs, you can avoid the taxes. Below are a few investment options:

- We assume that you have taken a Home loan to purchase the properties. Ensure that the interest payments on those are Rs 2 lakhs p.a.

- Invest in certain payable deductions u/s 80 C up to Rs 1,50,000 (Click here to know the details of such payments)

- Invest to get the deduction u/s 80D up to Rs 50,000.

- Invest to get the deduction u/s 80 CCD up to Rs 50,000.

- You can claim rebate u/s 87A and get tax liability to zero.

This is how your tax liability for FY 19-20 will look like:

[su_table]

| Income under the head Salaries | |

| Gross Salary |

10,00,000 |

| Less: Standard Deduction |

(50,000) |

|

Net Salary (A) |

9,50,000 |

| Income under the head House Property | |

| Notional rent |

NIL |

| Less: Interest on Home loan |

(2,00,000) |

|

Loss from the head house property (B) |

(2,00,000) |

|

Gross Total Income (A)+(B) |

7,50,000 |

| Less: Deductions | |

|

U/s 80C |

(1,50,000) |

|

U/s. 80D |

(50,000) |

|

U/s. 80CCD |

(50,000) |

|

Net taxable income |

5,00,000 |

|

Tax liability |

12,500 |

| Less: Rebate u/s 87A (Max) |

(12,500) |

|

Net tax payable |

NIL |

[/su_table]

She can be contacted at info.financepost@gmail.com

- How to do a transaction in Digital Rupee (CBDC-R)? – A Step by step Guide - 10/12/2022

- Can you rectify your 26AS? - 20/09/2022

- Tax implications on Cashback - 09/09/2022

Disclaimer: The above content is for general info purpose only and does not constitute professional advice. The author/ website will not be liable for any inaccurate / incomplete information and any reliance you place on the content is strictly at your risk.

Follow us on Social Media by clicking below

Follow @financepost_in

I am 74 years of age and my net income (Less Deducutions u/s 80C,80TTB)from Pension and Interest is Rs.439307.00. I have LTCG from Debt Fund at Rs.109840.00.Whether Rebate u/s 87A is to be calculated on normal income only as I need to pay tax separately on lTCG @20%? Kindly clarify.

You can avail the benefit of rebate u/s 87A and your tax liability will be zero as per the details provided above.

My long term capital gain on equity mutual funds (10%) is 16,55,675 and long term capital gain on debt mutual funds (20%) is 5,94,995, short term capital gain on equity (15%) is 51,671 but taxable value at normal rate is 4,15,218. Whether rebate under 87A will be available to me. System is not allowing rebate and tax on normal rate is computed as Rs.5761 including tax on special rate Rs.2.92,317.

You get a rebate when your total income including capital gain is Rs 5 lacs. In your case that is not the case hence the system is not allowing you rebate. Hope that clarifies your doubt

IamaResidentIndividual.govt.retd.MytotalIncome.is.506202.incl,LTCG8721forFY2021/22.canIavail.tax.benifit.u/s87A

If after availing the benefit of all the deductions available your income exceeds Rs 5 Lakhs then you are not eligible to claim the benefit of rebate u/s 87A.

For any further queries, you can reach out to us at info.financepost@gmail.com