FinancePost

Updates You Can Bank On

Home

GST

Income Tax

Finance

IPO

About Us

Contact Us

Terms & Conditions

Privacy Policy

News Ticker

[ 11/07/2023 ]

50th GST Council Meeting

GST

[ 01/04/2023 ]

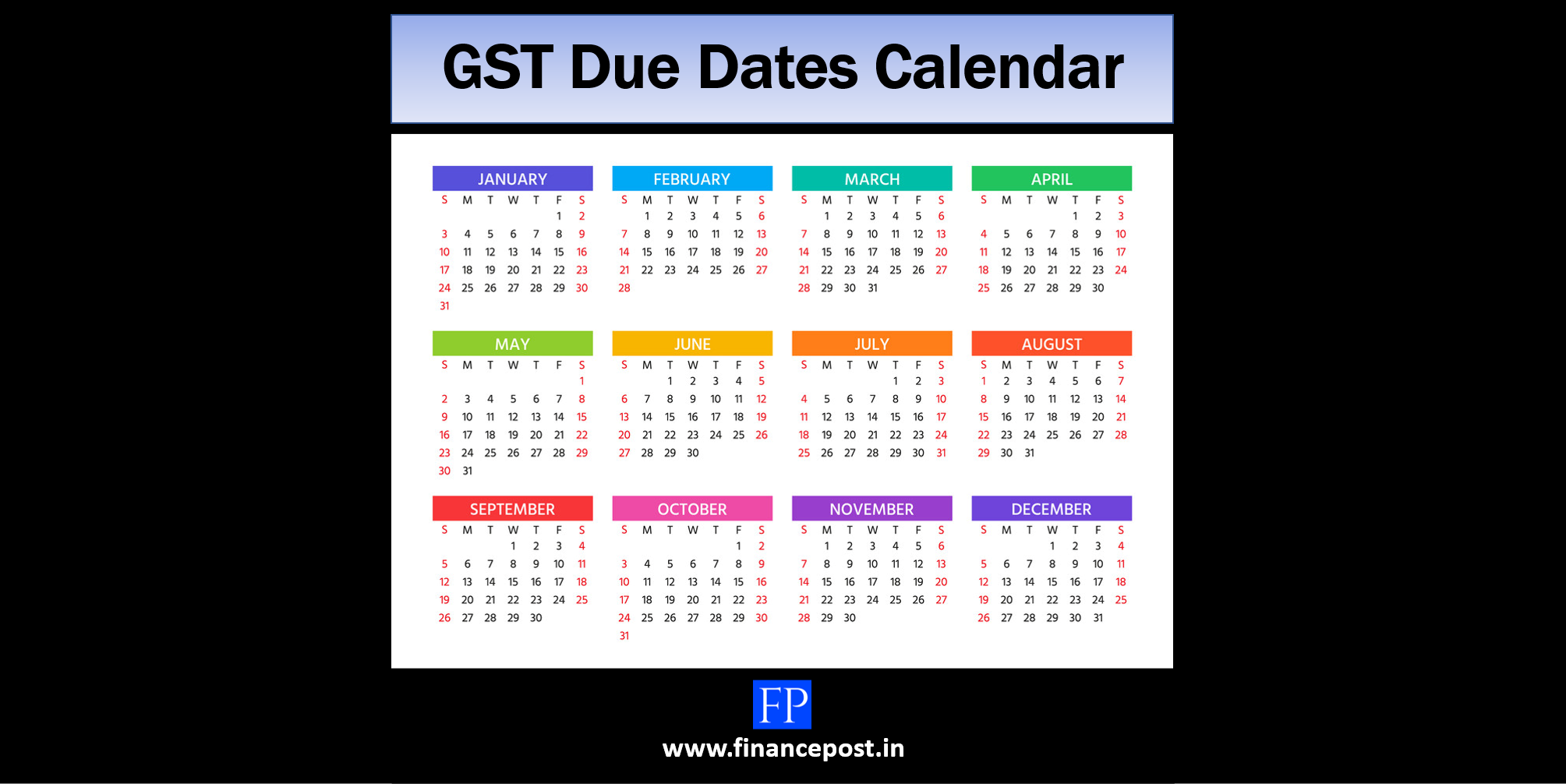

GST Compliance Calendar of October 2023

GST

[ 27/03/2023 ]

GST sections amended in Finance Act 2023

GST

[ 25/03/2023 ]

GST checklist with the onset of FY 2023-24

GST

[ 03/03/2023 ]

Final Return after cancellation of GST registration

GST

GST

50th GST Council Meeting

GST

GST Compliance Calendar of October 2023

GST

GST sections amended in Finance Act 2023

GST

GST checklist with the onset of FY 2023-24

GST

Final Return after cancellation of GST registration

GST

50th GST Council Meeting

11/07/2023

0

GST Compliance Calendar of October 2023

01/04/2023

4

GST sections amended in Finance Act 2023

27/03/2023

0

GST checklist with the onset of FY 2023-24

25/03/2023

2

Final Return after cancellation of GST registration

03/03/2023

8

49th GST Council Meeting

18/02/2023

0

ITC on CSR activities

02/02/2023

0

Gentle reminder! Apply for fresh LUT

01/02/2023

0

48th GST Council Meeting

05/12/2022

0

GST Annual Return Due Dates

01/12/2022

8

Income Tax

Tax on winnings from online games

04/02/2023

0

Tax Audit Report

21/09/2022

0

Can you rectify your 26AS?

20/09/2022

4

Income Tax applicability on HUF

18/09/2022

2

Refund Re-Issue Request

11/09/2022

4

Tax implications on Cashback

09/09/2022

0

Personal Finance

Union Budget 2023

01/02/2023

0

How to do a transaction in Digital Rupee (CBDC-R)? – A Step by step Guide

10/12/2022

0

India’s Digital Rupee

30/11/2022

2

UPI LITE

21/09/2022

2

Follow Us on Social Media

You May Also Want To Read

Important Announcements made by Finance Minister on 23 Aug 2019

23/08/2019

0

Quarterly GSTR 1

16/03/2022

0

FAQs – Filing of Income Tax Return

26/06/2019

0

Steps to change registered mobile number on the GST portal

03/02/2021

0

A checklist that all the tax deductions have been claimed for the year before filing ITR

25/02/2019

0

Trade Credit from foreign exchange perspective

08/09/2020

0

Follow Us on Twitter

Twitter feed is not available at the moment.

Like Us on Facebook

Join Our Whatsapp Group

Click above to receive regular updates

Copyright © 2024 | MH Magazine WordPress Theme by

MH Themes